The short answer: £1,000 gross per tax year – not per month, not per hustle, and not your profit. Your total sales before any deductions.

That is the UK’s trading allowance for 2026, and it is the most important number in UK side hustle tax. But the way it is worded in most online articles leaves out four things that regularly catch people out – things that turn an apparently safe £950 of Etsy sales into a surprise tax bill.

This article covers exactly what the threshold is, how HMRC measures it, what happens when you cross it, and how to calculate whether you actually owe any tax. It also covers the £3,000 change that is coming – and why you should not assume it is already in force.

The £1,000 Trading Allowance — What It Actually Means?

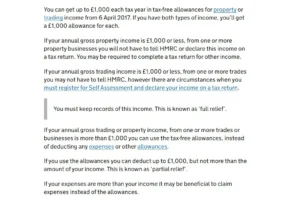

Every UK individual receives a £1,000 trading allowance each tax year. The tax year runs from 6 April to 5 April the following year, so the 2025/26 tax year ran from 6 April 2025 to 5 April 2026, and the 2026/27 tax year runs from 6 April 2026 to 5 April 2027.

The allowance works as follows:

If your total gross trading income, the total amount paid to you before any expenses, fees, or deductions, stays below £1,000 in the tax year, you owe no tax on it and do not need to register for Self Assessment or tell HMRC anything about it.

If your total gross trading income exceeds £1,000, you must register for Self Assessment, file a tax return, and pay any tax and National Insurance owed on your profits.

That is the core rule. Everything else is detail, but the detail matters enormously.

The Four Things Most Articles Get Wrong

Most guides on this topic leave out at least one of the following. All four directly affect whether you need to register and how much you owe.

One: The Allowance is Measured on Gross Income, Not Profit

HMRC does not look at what you kept. It looks at what came in.

If you sell candles on Etsy and your total sales for the year were £1,150, but you spent £600 on wax, wicks, packaging and Etsy fees, your gross income is £1,150, not £550. You have crossed the threshold and must register, even though your actual profit was only £550.

This is the single most common misunderstanding. People assume “I only made £400 profit” means they are safe. The profit figure is irrelevant for the registration trigger. What matters is the total amount people paid you.

Two: It Covers All Your Side Hustles Combined

The £1,000 is one allowance per person, not one per activity.

If you earn £700 from reselling on Vinted and £400 from occasional dog walking, your combined trading income is £1,100. You have crossed the threshold, even though neither activity alone did.

HMRC does not see separate businesses when it looks at a sole trader. It sees one person’s total self-employment income.

Three: It is Separate From Your Personal Allowance

The trading allowance (£1,000) and your personal allowance (£12,570 for 2025/26 and 2026/27) are two different things that serve two different purposes.

The trading allowance determines whether you need to register and report. Your personal allowance determines how much of your reportable income is tax-free.

If you are employed and your salary already uses up your personal allowance, every pound of side hustle profit above £1,000 will be taxed at your marginal rate 20%, 40%, or 45%, depending on your total income. The personal allowance will not save you again.

Four: Crossing £1,000 Does Not Automatically Mean You Owe Tax

Registration and tax liability are not the same thing.

Once gross income crosses £1,000, you must register and file. But whether you actually owe income tax depends on your total income picture, including your salary, other income, and how much personal allowance you have remaining.

Someone with no other income who earns £5,000 from their side hustle will pay no income tax at all (because £5,000 minus the £1,000 trading allowance = £4,000 taxable profit, which sits well below the £12,570 personal allowance). They still need to register and file, but their tax bill is zero.

What Counts as Gross Income (and What Does Not)?

Gross Income Includes

Every pound paid to you for goods you made or sourced to sell. Total Etsy, eBay, Vinted, Depop or other platform sales revenue. Everything paid to you for services, tutoring fees, dog walking payments, cleaning charges, freelance invoices. Delivery platform earnings (Deliveroo, Amazon Flex, Uber Eats).

Rental income if using the trading allowance route (though rental income normally has its own separate £1,000 property allowance and different rules, see the note below). Cash-in-hand payments are included exactly as if they were bank transfers.

Gross Income Does Not Include

Money you receive from selling your own personal possessions to declutter old clothes, furniture, and gadgets you used yourself. HMRC’s test is whether you bought or made the items specifically to sell for profit.

If you did not, it is not trading income. PAYE salary from employment. Pension income. Benefits. Savings interest (this has its own allowance). Cashback from cashback apps (this is a rebate, not income).

A Note on Rental Income

If you rent out a room or property on Airbnb, this falls under the property income rules, not trading income. There is a separate £1,000 property allowance for this, the same value but treated as an entirely separate allowance.

If your room is in your main home and total rental income is under £7,500/year, the Rent-a-Room scheme applies instead, which is more generous. These are different calculations, do not mix them with your trading income.

Do You Owe Any Actual Tax Once You Cross £1,000?

Crossing the £1,000 gross income threshold means you must register for Self Assessment.

Whether you owe any tax depends on three things working together:

- Your taxable side hustle profit (gross income minus either the £1,000 allowance or actual expenses whichever you choose)

- How much personal allowance you have left after your other income

- Whether your profit exceeds the National Insurance threshold

The Income Tax Calculation

Your taxable side hustle profit is added to your other income for the year. The combined total is assessed against your personal allowance (£12,570 for 2025/26 and 2026/27). Anything above the personal allowance is taxed.

- Basic rate taxpayers (total income between £12,571 and £50,270): 20% income tax on side hustle profit.

- Higher rate taxpayers (total income between £50,271 and £125,140): 40%.

- Additional rate taxpayers (over £125,140): 45%.

If you are already employed and your salary exceeds the personal allowance, which is almost everyone earning over £12,570, your personal allowance is already used up. Every pound of side hustle profit above the £1,000 trading allowance is taxed at your full marginal rate from the first pound.

National Insurance

Class 2 National Insurance was abolished for the majority of self-employed people from April 2024. You no longer pay a flat weekly NIC charge.

Class 4 National Insurance applies on profits above £12,570. The 2025/26 and 2026/27 rates are 6% on profits between £12,570 and £50,270, and 2% on profits above £50,270.

For most side hustlers with a main job, the salary already crosses £12,570, so Class 4 NIC applies to the side hustle profit from the first pound. This is often overlooked in tax calculations.

Voluntary Class 2 Contributions

Even though compulsory Class 2 NIC is abolished, you can still pay it voluntarily (£3.45/week for 2026/27) if your profits fall below £7,105. This counts toward your State Pension and qualifying years. If you are building pension entitlement, this matters particularly for younger side hustlers or those with gaps in their NI record.

Worked Examples — Three Real Scenarios

Scenario 1: Under the Threshold — No Action Required

Situation: Part-time employed, earns £18,000/year salary. Sells handmade pottery on Etsy and at craft fairs. Total gross sales in 2025/26: £730 (after adding up every sale).

Analysis: £730 is below £1,000 gross. The trading allowance covers it entirely. No registration needed. No tax return required. Keep records in case HMRC ever queries, but nothing to file.

Tax owed: £0.

Scenario 2: Just Over the Threshold — Employed With Salary

Situation: Full-time employed at £28,000/year. Does freelance graphic design in evenings. Total invoices raised and paid in 2025/26: £1,800 gross. Software subscriptions for design work: £180. Other expenses negligible.

Option A — trading allowance:

Taxable profit: £1,800 minus £1,000 = £800

Income tax at 20% (salary uses personal allowance): £160

Class 4 NIC at 6% (salary exceeds £12,570): £48

Total tax bill: £208

Net from side hustle after tax: £1,592

Option B — actual expenses:

Taxable profit: £1,800 minus £180 = £1,620

Income tax at 20%: £324

Class 4 NIC at 6%: £97

Total tax bill: £421

Decision: Option A (trading allowance) saves £213. Always run both calculations; the allowance is not always better.

Registration required? Yes, gross income exceeded £1,000. Registration deadline: 5 October 2026 (for 2025/26 tax year income). Filing deadline: 31 January 2027.

Scenario 3: No Other Income — Side Hustle Only

Situation: Recently left employment. Doing dog walking and pet sitting as only income from October 2025. Total gross earnings in 2025/26 (6 months): £5,400. Insurance and equipment costs: £290.

Option A — trading allowance:

Taxable profit: £5,400 minus £1,000 = £4,400

Personal allowance remaining: £12,570 (no salary to use it up)

£4,400 is below £12,570 — income tax: £0

Class 4 NIC: profit below £12,570 — NIC: £0

Total tax bill: £0

Option B — actual expenses:

Taxable profit: £5,400 minus £290 = £5,110

Same result – below personal allowance. Tax: £0

Conclusion: No tax owed in either case. But registration is still required because gross income exceeded £1,000. Must register, file a return showing £0 owed, and keep records.

Key insight: registration and tax liability are separate. You can have a zero tax bill and still be legally required to file a Self Assessment return.

The £3,000 Threshold — What is Changing and When?

You may have read that the trading allowance is rising to £3,000. The situation is more nuanced than most articles report, and getting it wrong can result in penalties.

What the Government Has Announced?

The government has stated its intention to raise the threshold above which a full Self Assessment tax return is required from £1,000 to £3,000.

This change would simplify reporting for lower earners, those earning between £1,000 and £3,000 from side hustles would still owe tax, but would use a simpler online tool rather than a full Self Assessment return.

This change is expected to remove approximately 300,000 people from the Self Assessment system. It is supported in principle across both main parties.

What Has Not Happened Yet?

As confirmed by ICAEW in their April 2026 tax guidance and multiple accountancy bodies, this change has NOT been legislated as of May 2026. No Royal Assent. No implementation date. No active system to use.

The £1,000 gross trading allowance remains the operative threshold for the 2025/26 tax year (deadline: 31 January 2027) and the 2026/27 tax year (deadline: 31 January 2028).

What This Mean for You?

If you earned over £1,000 gross in 2025/26 and have not registered, the current rules apply. Register by 5 October 2026.

Do not wait for the £3,000 threshold to be confirmed before registering. It has no legal effect until Parliament passes the necessary legislation. Acting on the assumption it is already in force is a significant compliance risk.

When the change does take effect, HMRC will publish clear guidance on gov.uk. Watch for announcements in future Autumn Budgets or Spring Statements.

What to Do if You Have Already Crossed the Threshold?

If you earned over £1,000 gross from side hustles in 2025/26 and have not yet registered, here is the correct sequence:

Step 1: Check Whether You Genuinely Crossed the Threshold

Add up every payment received from trading activity between 6 April 2025 and 5 April 2026. Be thorough, including cash, bank transfers, PayPal, platform payouts, and any kind of payment for services. Do not net off fees or expenses. If the total is under £1,000, you do not need to register.

Step 2: Register for Self Assessment

Go to gov.uk/register-for-self-assessment. Select “I am self-employed.” Have your National Insurance number ready. The process takes around 10 minutes. HMRC will post your Unique Taxpayer Reference (UTR) within 10 working days.

The registration deadline for 2025/26 income is 5 October 2026. Register as soon as you reasonably can. Do not leave it to October.

Step 3: Set Up Your Government Gateway Account

Your UTR is needed to create or link to a Government Gateway account. This is the portal through which you file your return. If you already have one for another reason (PAYE coding queries, child benefit, etc.), you can add Self Assessment to the same account.

Step 4: Gather Your Records

Before filing, you need the gross income figure and either your actual expenses or the decision to use the £1,000 trading allowance. Bank statements, platform payment reports (Etsy, eBay, Vinted, and similar platforms all provide annual summaries), and any receipts for claimable expenses.

Step 5: File by 31 January 2027

The online Self Assessment filing deadline for the 2025/26 tax year is 31 January 2027. Tax owed is due the same day. Filing early is always advisable it gives you time to budget for any tax due and avoids the January rush.

If You Have Missed Previous Years

If you have not registered for a year or more and earned over £1,000 gross, the correct action is voluntary disclosure. HMRC’s view of voluntary disclosure (you come forward before they contact you) is significantly more favourable than non-voluntary disclosure.

Penalties are typically much lower and interest charges are the main consequence. Go to gov.uk/make-a-voluntary-disclosure.

Frequently Asked Questions

What if I cross £1,000 in one month but end the year under £1,000?

The trading allowance is measured over the full tax year (6 April to 5 April). A strong month is irrelevant on its own. What matters is the annual total. If you earn £1,200 in November but nothing else all year, you have crossed the threshold. If you earn £900 spread across the year, you have not.

Can I split income with my partner to stay under £1,000 each?

Only if the income is genuinely earned by each of you. HMRC examines the economic reality of who did the work and who received the payment. Artificially splitting income to avoid the threshold is tax avoidance and carries a serious risk if challenged. If both of you genuinely trade (separate Etsy shops, separate clients, separate dog walking rounds), you each have a separate £1,000 allowance legitimately.

Does the allowance reset every tax year?

Yes. The £1,000 trading allowance is a per-year allowance. Crossing it in 2024/25 does not affect your 2025/26 allowance. However, once you are registered for Self Assessment, you remain registered and must file a return each year, even if your income drops below £1,000, until HMRC confirms you can deregister.

What about income from multiple platforms — does each get its own allowance?

No. The £1,000 is per person, across all platforms and all activities combined. £500 from Etsy + £600 from Deliveroo = £1,100 gross. You have crossed the threshold.

I run a side hustle jointly with a friend. How does the allowance work?

If you and a friend run a genuine business partnership, each partner’s share of income is assessed separately against their individual £1,000 trading allowance. A 50/50 partnership earning £1,600 total means each partner has £800 under the threshold for both, if those are the only trading activities for each of you. But partnership tax rules are more complex than sole trader rules. Consider speaking to an accountant if this is your situation.

My platform deducted fees before paying me. Do I use gross or net?

Gross. HMRC’s trading allowance test uses your total sales value, which customers paid, before the platform deducted its fees. If you sold £1,200 on Etsy and received £950 after fees, your gross income for threshold purposes is £1,200. You can then deduct the fees as an allowable expense if you are using Option B (actual expenses) instead of the trading allowance.

What to Read Next?

For the step-by-step process of actually filing your return once you have registered, see our guide: How to Declare Side Hustle Income to HMRC in 2026 (Step-by-Step).

If you need to understand the full tax picture, NICs, expenses, payment on account, and MTD, our complete UK side hustle tax guide covers it in full.

For profession-specific guidance on how the threshold affects your particular situation, see our side-by-side in the complete guide to UK side hustles.

More in Tax, Legal & HMRC

How to Declare Side Hustle Income to HMRC in 2026? (Step-by-Step)

If your UK side hustle earned more than £1,000 gross in the 2025/26 tax year or is on track to in 2026/27, you need to declare it to HMRC through Self Assessment. Not doing so is not an oversight HMRC will overlook. Since January 2026, platforms including Etsy, Vinted, eBay, Deliveroo and Airbnb have been […]